-

In early June 2026, ASML Holding was caught in a broader semiconductor sell-off after Broadcom’s guidance and stronger-than-expected US jobs data reset expectations for AI chip spending and raised concerns about higher discount rates.

-

This episode highlights how ASML’s share price can be impacted by sector sentiment and macroeconomic changes, even when its own fundamentals and regulatory trends are strong.

-

We now examine how this sector-wide reset in AI chip spending expectations affects ASML’s investment profile and perceived risk-reward balance.

AI Gold Rush’s 48 Best ‘Picks and Shovels’ Picks Leverage the AI Infrastructure Supercycle to turn record-breaking demand into massive cash flow.

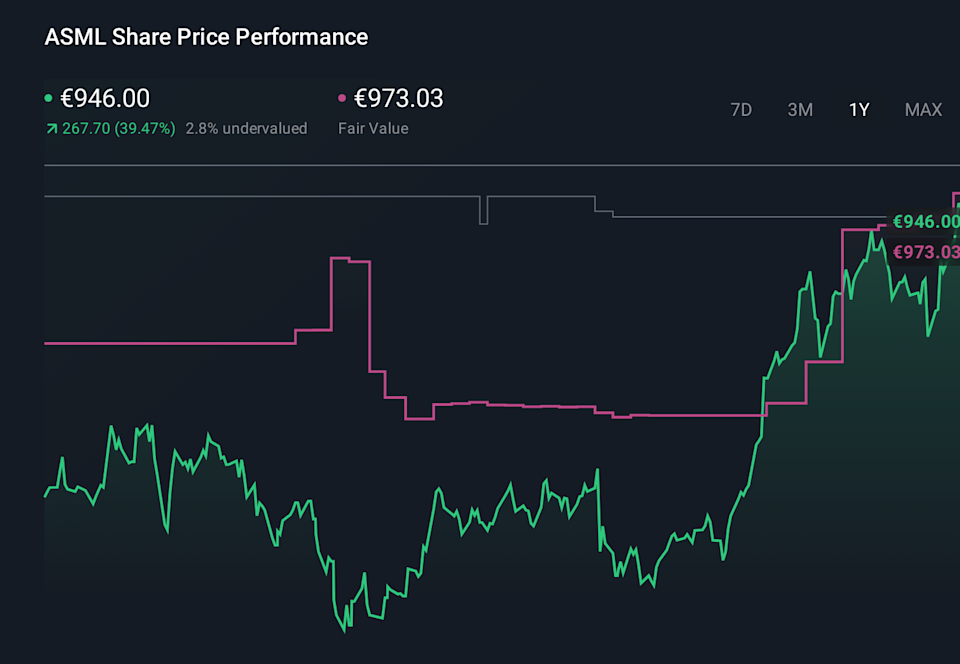

ASML HOLDING INVESTMENT STORY REVIEW

To own ASML, you have to believe that demand for advanced lithography tools coupled with AI and leading edge chips will be resilient through macro swings. The near term catalyst is how quickly customers convert EUV and futures high NA interest into firm orders and shipments. The recent sector-wide sell-off on AI spending and rate concerns has yet to change ASML’s order or guidance picture, so the underlying catalyst and key macro demand risk remain largely intact.

In that context, ASML’s April guidance for 2026 revenue of €36.0 billion to €40.0 billion, with strong Q1 results, feels particularly relevant. This underscores that customers are still accelerating capacity plans ahead of a pullback in sector sentiment, which is central to the elegant AI infrastructure narrative, but expectations for tool demand, especially at higher NA price points, may now be higher than hyperscalers and foundries are prepared to sustain.

Yet, beneath the enthusiasm for AI tools, investors should be aware of growing technological nationalism and trade barriers.

Read full details on ASML Holdings (it’s free!)

ASML Holding’s narrative projects revenue of €54.2 billion and revenue of €18.9 billion by 2029. This requires annual revenue growth of 17.1% and a revenue increase of around €8.9 billion from €10.0 billion today.

How ASML Holding’s projections provide a fair value of €1507, a 3% upside to its current price.

Exploring other perspectives

Some low-target analysts were already cautious, considering ASML revenue of around €42.8 billion and €14.7 billion in 2029, which contradicts current AI-driven optimism and reminds that views on export risks and demand for tools can change drastically as new information comes in.

#ASML #Holding #ENXTAMASML #gained #changed #chip #sentiment #reset #sector