The semiconductor sector experienced a brutal selloff last week, and it began Broadcoms (AVGO 7.49%) The latest quarterly earnings report on Wednesday evening. Despite posting a strong result, the company’s forward guidance fell short of Wall Street’s expectations, sending its stock down 20%.

Broadcom is a high-profile business with a strong demand pipeline for its artificial intelligence (AI) accelerators, which are customizable data center chips that have become a popular alternative to traditional graphics processing units (GPUs) offered by rivals. Nvidia. So, could the recent decline be a buying opportunity for investors? The answer may surprise you.

Image Source: Getty Images.

An impressive list of AI clients

Nvidia’s GPUs are the best data center chips for AI workloads, but also hyperscalers letters And Meta platforms are increasingly chasing more specialized solutions to meet their specific needs, so Broadcom helps them design and build custom AI accelerators.

Alphabet has a long-standing partnership with Broadcom that includes several generations of its AI data center chips, which it calls Tensor Processing Units (TPUs). Alphabet recently released the TPU 8t for AI training, which offers 3x the processing power of its previous generation (called Ironwood), and the 8i for AI inference, which offers an 80% improvement in performance per dollar. Without Broadcom, companies like Alphabet would be stuck in closed ecosystems with suppliers like Nvidia, with limited control over pricing and innovation.

Broadcom provides accelerators to leading AI start-ups such as Anthropic and OpenAI, which continue to diversify their hardware stacks to unlock as much computing power as possible. Anthropic is acquiring at least $21 billion worth of Alphabet’s TPUs through Broadcom, which will be phased in throughout 2026 and 2027.

But Broadcom is one of the world’s best suppliers of data center networking equipment. Its Tomahawk 6 Ethernet switch controls how fast data travels between chips and devices, making it the industry’s only 100-terabit solution. However, the company is now launching a new version Double ability.

Broadcom’s Q2 revenue growth accelerated, but guidance fell

Broadcom generated $22.2 billion in total revenue for the second quarter of its 2026 fiscal year (ended May 3), up 48% from a year earlier. That growth rate marked a significant acceleration from the first quarter’s close of 29% three months earlier, and the pace was largely driven by AI-related sales.

The company’s AI semiconductor revenue came in at $10.8 billion in the second quarter, representing a 143% year-over-year increase.Management’s guidance for the current third quarter (ending in early August) says AI revenue could grow an even faster 200% to $16 billion.

Today’s change

(-7.49%) $-31.39

Current price

$387.52

Key data points

Market Cap

$1.8T

Day limit

$386.37 – $410.32

52 week limit

$241.11 – $495.00

Vol

1.9M

Average Vol

25.3M

gross margin

65.66%

Dividend yield

0.64%

Investors are unlikely to be disappointed by any of the above numbers, but Wall Street expects Broadcom to forecast about $16.36 billion in AI semiconductor revenue in the third quarter. Additionally, CEO Hock Tan maintained the company’s fiscal 2027 revenue guidance for this segment of the business at $100 billion, whereas many analysts had expected an increase.

As “disappointing” forecasts have stunned Wall Street, demand for AI hardware is now on the horizon. If it does, investment returns from the semiconductor industry will go up considerably.

Despite the selloff, Broadcom stock isn’t cheap

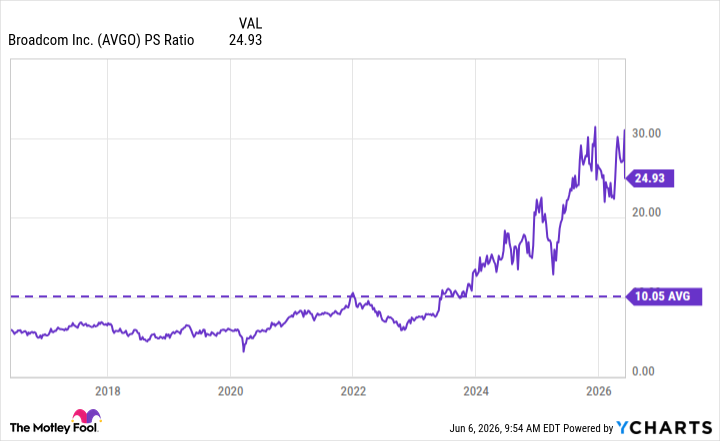

Although Broadcom stock closed 20% below its peak on Friday, June 5, it still trades at a whopping price-to-sales (P/S) ratio of 24.9, more than double its 10-year average of 10.1. This shows that investors are pricing in A lot Future earnings growth explains why the stock is so sensitive to even the hint that AI semiconductor sales are slowing.

AVGO PS ratio data by YCharts. PS Ratio = Price-Sales Ratio.

Also, based on Broadcom’s generally accepted accounting principles (GAAP) trailing 12-month earnings of $6.00 per share, its stock trades at a price-to-earnings (P/E) ratio of 64.1, nearly double the price. Nasdaq-100 Index, it has a P/E of 35.2. In other words, Broadcom appears overvalued relative to its basket of big-tech peers.

While there is currently a shortage of AI chips and components, there has been some disturbing news on the demand side recently, making investors nervous. Companies like Anthropic and the like Microsoft Recently introduced, passive pricing increases the use of their AI models and software, focusing more on consumption-based billing — and in Anthropic’s case, that’s counting consumption more aggressively.

These changes are necessary to cover the rising costs of data center hardware and electricity, but many companies are now rethinking their use of AI. Uber Technologies One of Anthropic’s customers, and its chief operating officer, recently said the ride-hailing giant was finding it difficult to justify its AI spending. Even Alphabet CEO Sundar Pichai said he was hearing complaints from many customers about rising AI costs.

If these rumblings translate into measurable reductions in AI software costs, demand for AI chips will almost certainly decline. That doesn’t bode well for Broadcom, so buying the recent drop in its stock right away isn’t a good idea, especially since its valuation is so high.

#Buy #Broadcom #Shares #Dip #answer #surprise #Motley #Fool